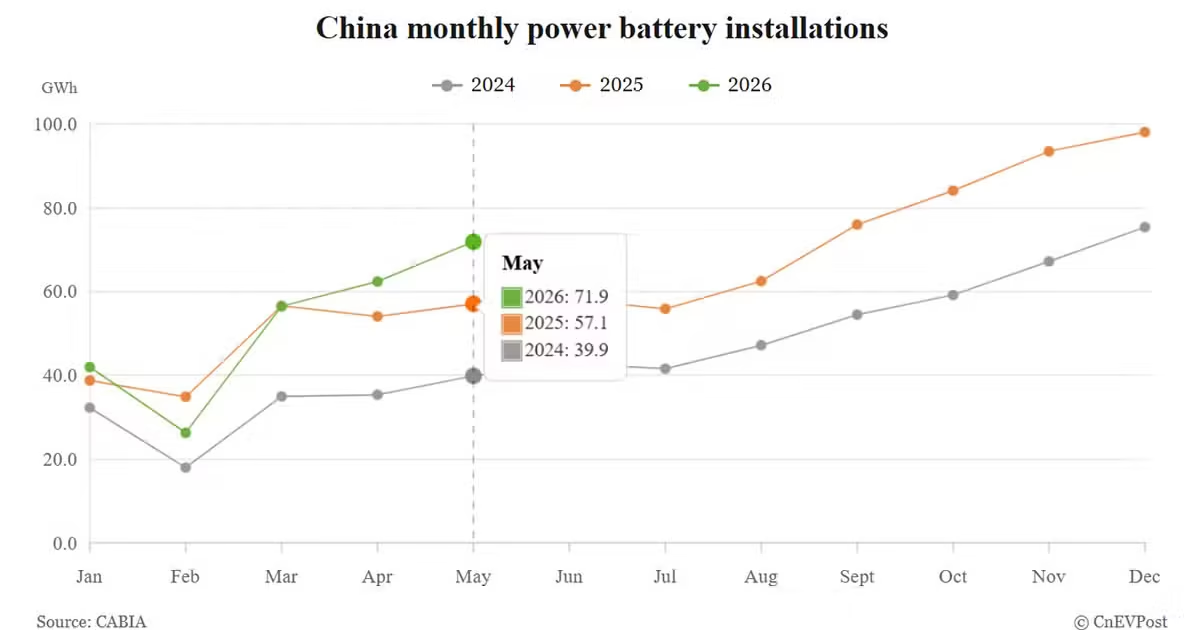

China’s electric vehicle battery installations surged to a record 71.9 GWh in May 2026, rising 25.9% year-on-year and 15.2% from April, according to data released by the China Automotive Battery Innovation Alliance (CABIA). The milestone was driven overwhelmingly by lithium iron phosphate (LFP) batteries, which accounted for 58.4 GWh — or 81.2% of all installations — as Chinese automakers and consumers continue to favor the cost-effective, thermally stable chemistry over ternary nickel-based alternatives.

LFP Tightens Its Grip: 81.2% and Growing

LFP batteries installed 58.4 GWh in May, up 25.4% year-on-year, while ternary (NCM/NCA) batteries reached 13.4 GWh, growing 27.3% year-on-year from a much smaller base. Over the first five months of 2026, cumulative LFP installations totaled 208.2 GWh (80.4% share), compared with 50.8 GWh for ternary batteries (19.6% share). The LFP dominance has been consistent and accelerating — May’s 81.2% share marks a new high, up from approximately 79% in the first quarter of 2026.

The structural shift toward LFP reflects several converging trends: CATL and BYD’s continued investment in LFP cell energy density improvements, automakers’ preference for lower-cost battery chemistries amid an industry-wide price war, and the growing share of mass-market and commercial vehicles in China’s NEV mix. LFP’s inherent thermal stability also aligns with tightening safety regulations following several high-profile EV fire incidents in 2025.

CATL at 46.14%, BYD at 16.56%: The Domestic Duopoly

CATL maintained its commanding lead in China’s passenger vehicle power battery market with a 46.14% share in May, though this represented a slight 0.51 percentage point decline from April, per CABIA data cited by CnEVPost. BYD — which primarily supplies its own vehicles — held 16.56%, consolidating its position as the second-largest player. Globally, CATL commanded 40.1% of the market in January-April 2026, while BYD held 14.2%, with seven Chinese companies collectively controlling 72.2% of the global power battery market.

The production side tells an even more dramatic story. Total battery production (including EV and energy storage) reached 191.7 GWh in May, surging 55.2% year-on-year — significantly outpacing the 25.9% installation growth rate. This production-installation gap of nearly 30 percentage points suggests either substantial inventory building by battery makers anticipating strong H2 demand, or growing export volumes that are captured in production data but not domestic installation figures.

Exports Surge: Batteries Become a Standalone Export Product

China exported 29.3 GWh of power and energy storage batteries in May, up 53.7% year-on-year. EV battery exports alone reached 20.1 GWh (+48.7%), while energy storage battery exports hit 9.2 GWh (+66.2%). Total battery sales — combining EV and storage applications — reached 182.2 GWh, up 47.4% year-on-year, with EV batteries accounting for 127.0 GWh and storage batteries contributing 55.2 GWh.

The export momentum underscores a structural shift in China’s battery industry: batteries are increasingly becoming a standalone export product rather than merely a component embedded in exported vehicles. European and Southeast Asian battery storage projects, in particular, are driving demand for Chinese LFP cells, which offer a compelling combination of cost, safety, and cycle life for grid-scale applications.

Why It Matters Globally

China’s record 71.9 GWh monthly battery installation — equivalent to roughly 700,000 average EV battery packs — demonstrates a scale of battery manufacturing and deployment that no other region can currently match. The 81.2% LFP share has profound implications for global battery supply chains: lithium, iron, and phosphate demand will continue to outpace nickel and cobalt demand, reshaping mining investment priorities worldwide. Furthermore, with CATL’s 46.14% domestic share and seven Chinese companies controlling 72.2% of the global market, Western efforts to build independent battery supply chains face an increasingly steep climb. The 55.2% production growth rate — nearly double the installation rate — suggests Chinese battery makers are building capacity for a global market that shows no signs of deceleration.

What’s Next

Industry attention now turns to whether battery installations can sustain this record pace through the seasonally stronger second half of 2026. Key variables include the trajectory of NEV sales (which fell 7.5% year-on-year in May despite record battery deployments), the commercialization timeline for solid-state batteries, and the evolving competitive landscape as second-tier Chinese battery makers like Gotion, CALB, and Sunwoda expand capacity. The CABIA will release June installation data in mid-July, which will indicate whether May’s 71.9 GWh record was a seasonal peak or the beginning of a sustained upward trajectory toward a 1 TWh annual run rate.

FAQ

Why is LFP dominating China’s battery market?

LFP batteries offer lower cost, better thermal safety, and longer cycle life compared to ternary (NCM/NCA) batteries. With CATL and BYD improving LFP energy density through innovations like cell-to-pack technology, the performance gap has narrowed, making LFP the preferred choice for mass-market EVs and commercial vehicles.

How does CATL’s 46.14% share compare globally?

CATL’s 46.14% domestic share in China’s passenger vehicle battery market is higher than its 40.1% global share (January-April 2026), reflecting intense competition from Korean and Japanese battery makers in overseas markets. However, CATL remains the world’s largest battery manufacturer by a wide margin.

What is driving the gap between battery production and installations?

May 2026 battery production reached 191.7 GWh (up 55.2% YoY), far exceeding the 71.9 GWh installed (up 25.9%). This gap reflects strong export demand (+53.7% YoY), growing energy storage applications, and manufacturers building inventory for anticipated H2 2026 EV demand.

Related Coverage

- CATL Sodium-Ion Battery Enters Mass Production, Targeting 160 Wh/kg by 2026 — The next battery chemistry entering the market

- Best EV Battery Technology 2026: BYD Blade vs CATL Qilin vs Tesla 4680 — Comprehensive comparison of leading battery technologies

Sources

- CnEVPost, China’s May EV battery installations jump 26%, extending growth streak — 71.9 GWh monthly record, LFP 81.2% share, YoY growth data

- CnEVPost, Top battery makers’ shares in China in May: CATL 46.14%, BYD 16.56% — manufacturer market share breakdown

- Gasgoo, China power battery installations reach record 71.9 GWh in May 2026 — CABIA monthly data report — production vs installation figures, export data